The post First Horizon Bank Bonus: $450 Checking appeared first on Best Wallet Hacks.

]]>First Horizon Bank is a commercial bank with locations in LA, NY, SC, TX, TN, AR, MS, AL, GA, KY, FL, NC and VA. If you live in one of those states, read on to learn about how you can get $450 for opening a new checking account.

First Horizon Bank has been around since 1864 and is FDIC insured (FDIC #4977), so your money is safe. They were founded in Memphis, TN but now have over four hundred branches manaing over $81.7 billion in assets, it is one of the oldest state chartered banks and one that is regulated by the Federal Reserve Board.

As a commercial bank, they offer the full suite of banking products from checking and savings to credit cards and loans. But today, I want to highlight the bank bonus available for their checking product.

Table of Contents

First Horizon Checking Bonus – $450

First Horizon has a really simple offer where you can get $450 if you meet a few simple conditions.

First, you need to be a new client and maintain an average daily collected balance of $5,000 in your total deposit balance AND make a minimum of 10 qualifying transactions for each statement cycle for the first three full statement cycles. A qualifying client-initiated transaction spans a lot of different transactions, including deposits, checks paid, ACH items, and signature and PIN-based purchases made with a First Horizon Debit Card.

That’s it!

No other requirements to get the $450 cash bonus. It’s quite simple.

The offer page does say that the “Offer is only available to the addressee of the offer, is non-transferable, may not be combined with other offers, and is only available for new clients that have not had an account at First Horizon within the last 12 months.” But you can get an offer code if you enter your information on the page we link to below.

This offer is available in LA, NY, SC, TX, TN, AR, MS, AL, GA, KY, FL, NC and VA.

There is a $2 monthly fee but easily waived if you opt for electronic statements plus you need to keep the account open for six months or you forfeit the bonus.

(Offer expires 4/30/2024)

How Does This Bonus Compare?

This bonus offer is really appealing because:

1. it doesn’t require a direct deposit, and

2. the deposit balance requirement is only $5,000

You get a “9% return on your deposit,” so to speak, and you just need to make 10 qualifying client-initiated transactions for each statement cycle for the first three full statement cycles – so about three months.

Here are a few other offers:

Barclays – $200

Barclays Bank will give you a $200 if you open a new savings account and deposit $25,000 or more within 30 days and maintain at least $25,000 for the next 120 days. The savings account also pays a competitive interest rate of 4.35% APY while you wait.

BMO Relationship Checking – $400

BMO Bank is offering a $400 bonus* when you open a BMO Relationship Checking and when you have at least $7,500 in qualifying direct deposits within the first 90 days. It is a very straightforward offer that is available nationwide.

*Conditions apply

Bank of America – $200 Bonus Offer

Bank of America offers a $200 Bonus Offer cash bonus if you open a new account and Set up and receive qualifying direct deposits totaling $2,000 or more into that account within 90 days of account opening. It has a monthly fee that is easy to have waived.

Chase Total Checking® – $300

Chase Bank will give you $300 when you open a Total Checking account and set up and receive direct deposits totaling $500 or more within 90 days. There is a $12 monthly fee that is waivable with a monthly direct deposit of just $500, so no gotchas on this deal!

HSBC Premier Checking – up to $4,000

HSBC has an offer where you can get up to $4,000 for eligible new customers who open an HSBC Premier checking account, make a sizable deposit, and make recurring monthly qualifying direct deposits of at least $5,000 for 3 consecutive months.

The post First Horizon Bank Bonus: $450 Checking appeared first on Best Wallet Hacks.

]]>The post NorthOne Business Banking Review: Low Fees for Business Owners appeared first on Best Wallet Hacks.

]]>Small business owners and sole proprietors can have a tough time finding bank accounts that don’t charge astronomical fees. This NorthOne review shares why small business owners have an attractive option with NorthOne.

The deposit account comes with a variety of features perfect for small business owners, including the ability to pay invoices, integrate with accounting software and Shopify and Etsy, and set up sub-accounts for easy money management.

At a Glance

- Standard account has unlimited mobile check deposits and no monthly maintenance fees.

- NorthOne Plus costs $20 per month and comes with reduced fees and priority customer service.

- Integration with accounting software like FreshBooks and QuickBooks.

- No physical branches or paper checks.

Who Should Use NorthOne?

NorthOne works with nearly all types of small business owners. However, they likely won’t have the capability to handle a large corporation’s banking needs.

However, if you’re a sole proprietor, freelancer, or are running an S-corp or other small business, NorthOne might work well for your banking needs.

Between the low fees and features like bill pay and sub-accounts, it should cover most banking needs for small business owners who can conduct their businesses entirely online.

If you prefer in-person banking and/or need paper checks, NorthOne is not for you.

NorthOne Alternatives

| Monthly Fee | $0 | $0 | $0 |

| Minimum Deposit | $0 | $50 | $0 |

| Paper Checks | Yes | No | Yes |

| Learn More | Learn More | Learn More |

Table of Contents

- At a Glance

- Who Should Use NorthOne?

- NorthOne Alternatives

- What Is NorthOne?

- NorthOne Business Banking Services

- Business Bank Account: Deposits and Bill Pay

- Sub-accounts with Auto-transfer Capabilities

- Accounting Software Integration

- Payment Processor Integration

- NorthOne Fees

- How to Open a NorthOne Account

- NorthOne vs. Bluevine

- NorthOne vs. Novo

- NorthOne vs. Axos

- FAQs

- Summary

What Is NorthOne?

NorthOne was founded in 2016 and officially launched to the public in 2019. It is not actually a bank, but a financial tech company. Its deposit account is backed by The Bancorp Bank and is FDIC-insured through Bancorp.

NorthOne’s Connected Bank Account is a demand deposit account that was created specifically for small business owners. It can work with all types of small businesses, including freelancers, sole proprietorships, and small corporations.

The NorthOne account has a long list of features for managing your business’s finances. These include automated tasks to help you more easily close your books at the end of the month.

The NorthOne mobile app gives you full control over your business finances so you can run your business from anywhere there’s internet access.

NorthOne Business Banking Services

Here’s a rundown of some of NorthOne’s most prominent features and how they can help your business.

Business Bank Account: Deposits and Bill Pay

With a NorthOne business bank account, you can:

- Make unlimited, fee-free mobile check deposits

- Send up to $10,000 per day by ACH transfer

- Send up to $200,000 per day by domestic wire transfer

- Receive unlimited ACH and wire deposits

- Receive debit cards for every business owner

As NorthOne is not a physical bank, you won’t have access to in-person services or receive any paper checks with a NorthOne account. All account transactions are conducted online or at an ATM.

However, you can still send paper checks to vendors within the U.S. through NorthOne — they will send a pre-funded paper check on your behalf for a fee of $1 per check (although this fee can be waived if you sign up for NorthOne Plus for $20 per month).

If you need to deposit cash, you can do so free of fees at the cash register of most Walmart, Walgreens, CVS, RiteAid, and 7/11 locations.

You can withdraw cash up to five times per day, for a maximum of $2,000 per day, from ATMs in the Mastercard, Maestro, or Cirrus ATM network.

Sub-accounts with Auto-transfer Capabilities

One of my favorite features of the NorthOne account is the sub-account feature. NorthOne has sub-accounts called “envelopes” that allow you to divide your business funds into different categories for easier money management.

For instance, you could have sub-accounts for categories such as:

- Payroll

- Paying taxes

- Emergency savings

- Future purchases, expansions, or growth

- A variety of business expenses

The NorthOne account allows for unlimited sub-account envelopes at no extra charge. Designed much like a personal financial envelope budgeting system, NorthOne’s envelopes help ensure your business has money set aside when it’s needed.

Bonus: You can set up auto-transfers for your envelopes to make setting aside money for specific expenses or savings even easier.

Accounting Software Integration

NorthOne has integration abilities with accounting software such as:

- QuickBooks

- FreshBooks

- Wave

After you connect your NorthOne account to one of its compatible software programs, you can import your chart of accounts. Then you can sync all of the information and transaction details between NorthOne and your accounting platform to help you easily manage your business income and expenses.

In addition, the company partners with both Shopify and Etsy and allows you to link those accounts to your NorthOne account. This means you can see all of your order numbers and the coordinating payments with either of those e-commerce platforms right on your NorthOne account.

Payment Processor Integration

NorthOne also integrates with several payment processing companies, including:

- PayPal

- Venmo

- Stripe

- Square

Partnership with these platforms means you can accept payment from any of these payment processors and have the money deposited directly into your NorthOne account.

NorthOne Fees

When you open your NorthOne account, you’ll be required to deposit $50. After that, there are no minimum balance requirements.

NorthOne has two plan options. All customers are first assigned to the NorthOne Standard plan, which has no monthly account fees. However, you can choose to upgrade to NorthOne Plus for $20 per month. With this plan, you get reduced fees and priority customer support.

With NorthOne Standard, fees are as follows:

- 1.5% on same-day ACH transfers, up to a $15 maximum

- $1 per check for sending physical checks

- $0.50 on bill payments

- $20 for sending or receiving domestic wires

By comparison, with NorthOne Plus there are no fees on ACH transfers, physical check sends, or bill payments. Sending a domestic wire costs $15, while receiving still costs $20.

Regardless of which plan you’re on, NorthOne won’t charge you for using in-network ATMs. However, the ATM owner may charge you a fee — even if you’re using an in-network ATM.

How to Open a NorthOne Account

Signing up with NorthOne is fairly simple and can be done in just a few minutes. Here’s the information you’ll need to open your account:

- Valid government-issued photo ID

- Valid phone number

- Social Security number

- Employment insurance number (for LLC, S-corp, C-corp, and Partnerships)

- Home and business address

- Details about your business and owner(s)

NorthOne’s customer service team can help via chat, email, or phone. The hours for the customer service center are Monday to Friday, 9 a.m. to 6 p.m. Eastern time.

NorthOne vs. Bluevine

Bluevine Business Checking offers features for small business owners that include:

- $0 monthly fee

- 2.00% APY interest paid on account balances up to $100,000

- Paper checks

- No minimum balance

- $0 initial deposit requirement

- $0 fees for non-sufficient funds

There are unlimited transactions with the Bluevine account. And you can use MoneyPass ATMs for free. You can make cash deposits at GreenDot locations, but you’ll pay $4.95 per deposit for doing so.

Online bill pay is free with Bluevine as well. Note that there are no in-person banking capabilities with Bluevine.

Bluevine’s website doesn’t clearly list partner integrations, so you’ll have to call customer service for information on partner integrations for your business.

Check out our full review of Bluevine.

NorthOne vs. Novo

The Novo Business Checking account includes the following features:

- $0 monthly service fee

- $50 minimum initial deposit

- No minimum balance

- ATM fee refunds up to $7 per month

- Novo reserve accounts

Note that there are no paper checks and no in-branch banking.

With Novo, you can invoice customers for free using the Novo app. You can even set recurring invoices. Novo also offers online bill pay. Integrations include QuickBooks, Amazon, Shopify, Xero, and more.

Incoming domestic and international wire transfers are free with Novo. Novo doesn’t allow outgoing domestic wire transfers but uses the ACH transfer system instead. You can send outgoing international wire transfers from your Novo account, but Novo partners with Wise to do so and you’ll pay applicable fees.

Bonus feature: Novo offers software discounts on many business software programs. See the Novo website for specific information on these discounts.

Check out our full review of Novo Business Checking.

NorthOne vs. Axos

Features of the Axos Basic Business Checking include:

- $0 monthly service fee

- $0 minimum deposit

- $0 minimum balance

- $0 fees for in-network ATMs

- Paper checks

- Unlimited transactions

Axos offers separate business savings accounts and money market accounts as well. If you don’t care for the sub-account option where monies are tied to the main account but categorized, you might prefer Axos Bank for your business banking.

Also, while the Basic Business Checking account doesn’t pay interest, Axos does offer a high-yield Business Interest Checking account.

This account will pay interest on balances, however, there is a $10 monthly fee if your balance is below $5,000. The Business Interest Checking also features ATM fee reimbursements and an initial opening deposit minimum of just $100.

Check out our full review of Axos.

FAQs

NorthOne is a financial technology company, not a bank. However, deposits into your NorthOne account are FDIC-insured through The Bancorp Bank.

NorthOne does not have any physical locations. It is an online-only fintech company. All transactions with NorthOne are done digitally from your phone or computer or at an ATM.

Eytan Bensoussan is the CEO and co-founder of NorthOne. He founded the company in 2016 with Justin Adler.

Summary

Having the right bank account for your business is so important. Small business owners often have a tight budget and can’t afford to be lackadaisical about banking fees. Plus, small business owners can reap huge benefits from automated systems and smart partner integrations.

NorthOne offers low fees, bill pay capabilities, and integration with a wide range of accounting software and e-commerce platforms. If you’re good with banking that is entirely digital, NorthOne may serve your needs — just be sure to compare other business bank accounts before committing, to find the one that’s best for you.

The post NorthOne Business Banking Review: Low Fees for Business Owners appeared first on Best Wallet Hacks.

]]>The post Ownwell Review 2024: Property Tax Appeal Service appeared first on Best Wallet Hacks.

]]>How much are your property taxes?

In our county in Maryland, we pay a total of $1.442 per $100 of assessed value.

1.442% doesn’t sound like a lot, but the median home price in my county is around $580,000.

That’s $8,400 a year.

When I received my property tax assessment last year, it included a significant increase in assessed value. We renovated a section of the house, so part of that was justified, but it seemed like the jump was too high.

I decided to contest my property taxes myself and won. The process, which you can read about in the linked article, took several hours spread across several weeks. And I was “lucky” in that I was given a good result at the first stage (just filling out a form), so I accepted it.

If they rejected my claim and required me to plead my case to a live panel, I’m not sure I’d be as comfortable doing that.

Fortunately, there are services out there that will do it for you.

One of those is called Ownwell.

At A Glance

- Ownwell will appeal your property taxes on your behalf

- Monitors for tax exemptions based on your individual property

- No upfront fees – pay only upon successful reduction of property taxes

- Pay 25% or 35% of savings, depending on your state

- Available in California, Florida, Georgia, Illinois, New York, Texas, and Washington. (but expanding all the time so check your state)

- Average savings is $1,148

Who Should Use Ownwell

Homeowners and Real Estate investors who want to ensure they aren’t overpaying their property taxes should consider Ownwell. They will appeal your property taxes for no upfront costs and you pay a percentage of your savings if your appeal is successful. So there is no risk and no leg work for you.

Table of Contents

Who Is Ownwell?

Ownwell is a service that will contest your property tax assessments with your taxing authority so you can pay less in property taxes. They will also find exemptions and other tax savings you may not know about or have overlooked.

Ownwell was founded by Colton Pace and Joseph Noor in 2020. Pace’s background in investing and asset management gave him exposure to the various tools used by real estate investors, and he wanted to bring them to regular homeowners. The result is Ownwell, a service to contest property taxes.

Ownwell doesn’t operate in every state (yet).

In Which States Does Ownwell Operate?

Ownwell isn’t in every state and for some of the states they do operate in, they aren’t in every single county.

As of April 2024, they are in California, Florida, Georgia, Illinois, New York, Texas, and Washington. You have to double check that your county is included (it’s not feasible to list every county here though, California has 58 counties and Texas as 254!).

They are adding counties all the time, so the best way to know is to go to Ownwell and enter your address.

When Can I Appeal My Property Taxes?

The schedule for when you can appeal will depend on your state and, in some cases, the county within that state. They’re all on different schedules.

For example, in Maryland, this process only happens once every three years. In New York, and many other states, it happens every single year!

I asked Ownwell to provide a schedule (and they did) but it’s a little complicated and hard to share on a single screen… also, many dates are county specific and they cover so many counties that it’s unwieldly to list it all here.

The end result is that the simplest thing to do is sign up for Ownwell and then wait for your assessment to arrive. Then, enter in the details and decide whether you should use them to contest your appraisal.

As there’s no cost to sign up, you can use their technology to help you manage the schedule and decide later if you want to use them.

How Does Ownwell Work?

First, go to Ownwell and enter your address.

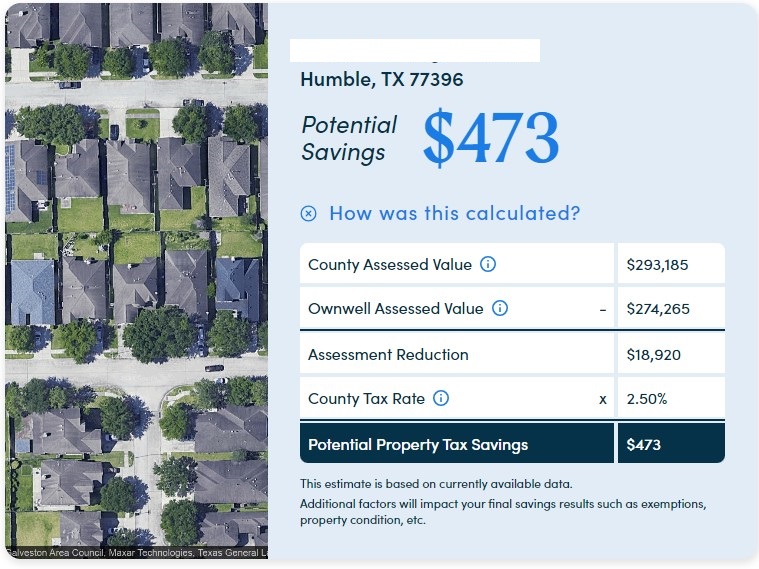

Since they don’t operate in Maryland, I chose a random property in Humble, TX (a suburb of Houston). They service Harris County.

It may not be worth it for a homeowner to learn the ins and outs of protesting property tax assessments for $473, especially if it’s not a guarantee you’ll get any reduction. But if I owned this home and didn’t want to do it, I’d be perfectly happy hiring someone on a contingency basis (I pay only if they win) – which is how Ownwell works (more on fees later).

If you continue, you’ll be prompted to enter your information. (I’m using a demo account, if you do this yourself, enter your information)

The next few screens confirm information, like whether you purchased this property in the last 18 months and the property owner’s name.

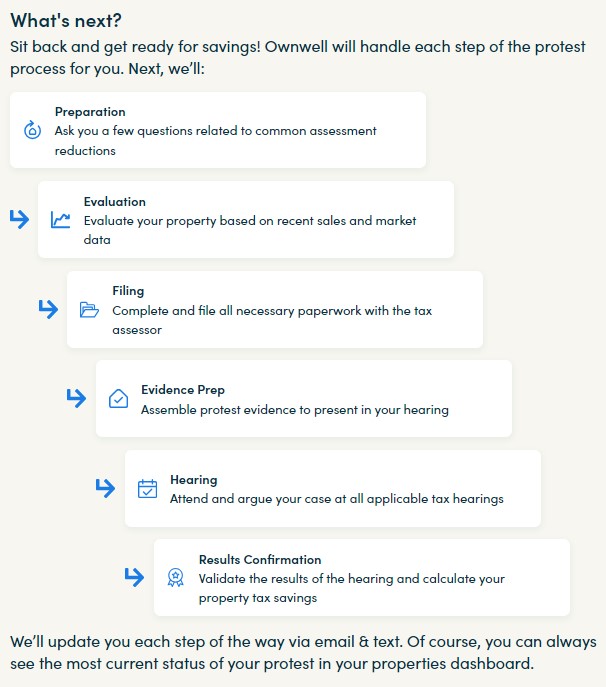

The last page, after you’ve confirmed all the details, authorizes Ownwell to act as your Tax Agent. This lets them contact the taxing authority on your behalf and contest your property taxes.

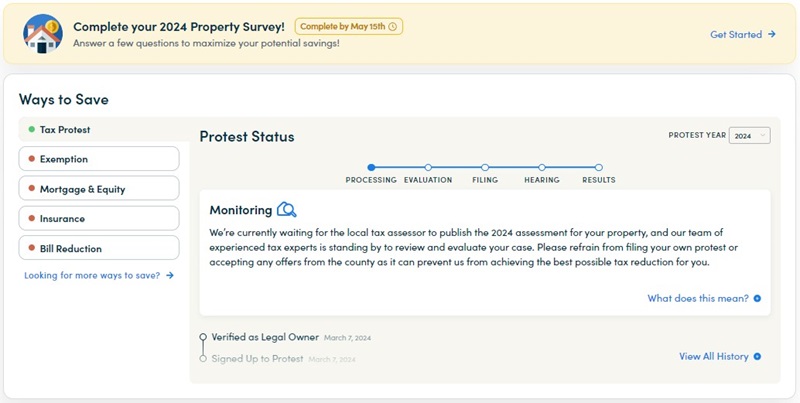

From here, you can log in and check the progress of your protest.

As of this writing, Texas hasn’t yet published the 2024 assessments, so Ownwell has nothing to do. I believe Texas publishes them in April, and then you have 30 days to protest.

This will vary from state to state and in Texas, you can do this every single year.

Finding Exemptions and Claiming Refunds

In addition to contesting your assessment this year, they offer a service to determine whether you’re eligible for any tax exemptions. If they find any, they can even make claims on previous years to get a tax refund.

There are a lot of different tax exemptions out there and these are challenging to keep track of. For example, here in Maryland, we have an Agricultural Use Assessment that significantly lowers property taxes on areas where you have agreed to keep to agricultural use. I only knew about it because the previous owner had it.

We don’t grow anything (commercial) on the land, it’s all wooded, but that counts. The only requirement is that we get an arborist to certify an agricultural use plan every few years, and we get a huge discount on the assessed value of the undeveloped land. It has saved us thousands of dollars a year.

Ownwell looks for exemptions like that.

Then, they will monitor your taxes each year to make sure everything is correct. If, for whatever reason, an exemption is left off, they’ll make sure to fix it.

Ownwell Fees

Ownwell operates on a success fee model – you only pay them if they win an appeal and lower your property taxes. They only charge you if your final property tax bill is reduced and they have a signed document from your taxing authority to prove it.

If they aren’t able to lower it, you pay nothing.

In California, New York, and Florida, the success fee is 35%. It is just 25% everywhere else.

For the above example, if Ownwell gets a $473 reduction in property taxes, I would pay them $118.25. I keep $354.75.

How does this fee compare to other companies? You should research this for your own state, as it will vary, but I found a tax firm in Texas that listed their pricing. On a single property, they charged 40% with a $149 minimum. For 2-5 properties, it was 35% with no minimum. Only 6+, it was 30%.

What are Ownwell Alternatives?

The biggest alternative is to call a local law firm that specializes in this same type of work. There are plenty of law firms that offer this. At this time, I’m not aware of a company that operates in multiple states.

The tradeoff with using a local law firm has to do with cost. They are typically not going to be able to work with individual homeowners and still be able to charge a small success fee. They often have minimum fees and will only take your case if they see it as being “worth their time.” In a quick search myself, I found that firms are very up front about this because contesting appraisals is time intensive and they don’t want to waste their time or yours.

As I mentioned in the above section about fees, I found a tax firm that charged 40% fee with a $149 minimum. In Texas, Ownwell charges just $25 with no minimum.

Alternatively, you can reach out to your real estate agent to see if they can help. This will be dependent on how friendly and available your agent is to this type of help. Some may do it for free, seeing it as a part of their offerings, while others won’t.

Is Ownwell Worth It?

It depends on how much you value your time and how much of a return you expect to get. If I owned a home in which a protest was going to net me $500 and it’s something I have to do every year, I’d more more likely to pay Ownwell a 25-35% success fee to handle it all for me. With four kids and a slew of other responsibilities, the ROI on my time just isn’t there.

Also, the property tax assessment process varies from state to state. In Maryland, we only have to do it once every three years and I had a personal interest in learning the process (also, I was happy after the first round reduction – the work gets considerably more involved after the first round). I realize I’m a weirdo like that, most people don’t care and just want to save money.

The only thing I do know is that you must contest your property tax assessment. You may not win a reduction, but you have to do it. Those increases will compound so you have to keep the increases as little as possible.

If you aren’t going to do it yourself, getting someone else to do it is better than taking the increase.

FAQs

Yes, Ownwell is a legitimate company that will appeal your property taxes for no upfront fee.

You absolutely can appeal your property taxes on your own. Assuming you have the time an inclination to research and file the appropriate documents. It took me a few hours of research, and I was successful in the first appeal.

Summary

Ownwell is a company that will appeal your property tax bill on your behalf with no upfront fees. You’ll pay either 25% or 35% (depending on your state) of the savings they can get you. If they are not successful at lowering your property tax bill, then their services are free.

The post Ownwell Review 2024: Property Tax Appeal Service appeared first on Best Wallet Hacks.

]]>The post Everyday Life Insurance Review 2024 appeared first on Best Wallet Hacks.

]]>Most of the time when you apply for life insurance, you’re working with a single company that offers policies directly. But if you want to find the best possible policy, you may decide to get quotes from multiple sources.

An easy way to collect multiple quotes is to apply with an insurance broker, which has access to several different providers and can get you multiple quotes with just one application.

Interested? That’s where Everyday Life comes in.

At a Glance

- Sorts through different insurance providers for customized quotes

- Offers automatic laddering strategy to help you save money

- Policies available for those up to age 85

Who Should Use Everyday Life?

If you’re planning to buy life insurance but want to review multiple quotes before committing to a single provider, Everyday Life may be for you. And since they offer automated laddering, it’s also a good option if you’d rather have someone else do the math on how much insurance you actually need over time.

However, if you’d like a more hands-on approach to choosing your insurance provider or, if you already have a chosen provider in mind, you may not need to rely on Everyday Life.

Learn more about Everyday Life

Everyday Life Alternatives

| Monthly Premium | Starts around $8 | Starts at $5 | Starts at $11 |

| Coverage Amount | $100,000 to $5 million | $100,000 to $8 million | Up to $1.5 million |

| Term Lengths | 10 to 30 years | 10 to 30 years | 10 to 30 years |

| Learn More | Learn More | Learn More |

Table of Contents

What Is Everyday Life?

Everyday Life partners with insurance companies to provide term life access to consumers. They are partnered with several companies, including Legal & General, SBLI, Fidelity Life, and more.

When you fill out the initial application, Everyday Life will determine what coverage you need. Your ideal coverage amount depends on several factors. For example, if you have many dependents who rely on your income, you’ll likely need more coverage than someone who is married without any kids.

Your health rating can also have a huge impact on your monthly premiums — and if you’re even approved for life insurance. For example, smokers will usually pay higher premiums than non-smokers.

Everyday Life’s Predictive Protection Laddering

What sets Everyday Life apart from other insurance providers is that they use a Predictive Protection model to decide exactly how much life insurance you need at any given point. One aspect of life insurance that people don’t always realize is that you don’t always need the same amount of coverage.

For example, let’s say you have two young children still in elementary school. While they’re young, you may want more coverage to pay any expenses that they have. But once they graduate college, you won’t be financially responsible for them anymore.

Also, you may have already paid off your mortgage by that time. These two factors mean that you likely won’t need as much life insurance as you did when you were younger.

This model can save you money because you won’t be paying for a policy you don’t need. This strategy is also known as laddering. You can ladder your policies manually with any insurance company. However, Everyday Life does the math for you.

They claim this model can save you up to 50% in premium costs over the entire policy life.

The right amount of coverage helps you avoid wasting money by overpaying, and it also guarantees your family’s needs will be met should the worst happen.

Learn more about Everyday Life

How Everyday Life Works

When you visit Everyday Life’s website, you will be asked basic questions, such as your ZIP code, birthdate, if you have ever used nicotine, and your annual income.

Once you complete this initial application, you will find out if you have been tentatively approved for a policy. You will also see which carriers are available and how much life insurance coverage Everyday Life recommends. However, you can always choose to purchase more or less coverage.

It’s important to note that the first part of this application is anonymous. However, you should answer the questions as accurately as possible. When you proceed to the real application, your information will be checked against your medical information and personal records. If you lie on the application, your final rate may be far off your initial quote.

Sometimes, you may be able to fill out an application online, whereas other times, you may be required to answer questions over the phone.

Everyday Life also says that most applicants can avoid getting a medical exam, but this may not apply to everyone.

Once you decide to get your official quote, you will have to provide your full legal name, email address, and phone number.

How Much Does Everyday Life Cost?

Because Everyday Life is a brokerage and not a direct insurance provider, it’s hard to guess exactly how much you will pay. Every insurance company has its own pricing algorithm that determines your monthly premium.

Another important thing to keep in mind is that everyone’s policies are priced according to their needs, as well as their age and current health status.

There’s no fee to use Everyday Life itself. You’ll only pay once you’ve confirmed a plan with your chosen insurance provider and set your monthly premium.

Learn more about Everyday Life

Everyday Life vs. Fabric

Fabric is a life insurance company primarily marketed to parents with young kids. Fabric’s term life policies range from $100,000 to $5 million, which is on the high end of what other life insurance companies offer.

Terms last between 10 and 30 years. Monthly premiums start around $8 for a typical policy for a 25-year-old.

Fabric lets you complete an application via their mobile app or on a browser. They have both Android and iPhone apps, both of which have high user ratings.

Fabric received an A+ financial strength rating from A.M. Best, which reviews insurance companies. This means that if you have to redeem your policy, the company will have the funds to pay you.

Fabric also offers life-planning services, like creating a will, setting up a Uniform Gifts to Minors Act (UGMA) account, and more.

If you change your mind, you can cancel the policy within the first 30 days and get a refund.

Everyday Life vs. Ladder

Ladder life insurance is named after the laddering strategy in which you can buy different policies to ensure that your life insurance matches your changing needs. According to Ladder, policies start at $5 a month, and you can buy coverage from $100,000 to $8 million, one of the highest limits on the market.

Ladder often lets you forgo the medical exam unless you buy a policy worth more than $3 million. Ladder knows that as your life changes, your insurance needs may decrease. As such, they will let you step down your coverage as you age, so you don’t have more insurance than you need.

If you have a Ladder term life insurance policy, you can reduce your coverage at any point. The company claims that you may be able to save thousands.

Unlike Everyday Life, Ladder requires that you ladder your policy manually. While this may require more work, it also gives you more control so you can keep more coverage if you want to.

Everyday Life vs. Bestow

Like the other companies on this list, Bestow is a direct life insurance provider. Their coverage amounts are lower than what Ladder and Fabric offer; their largest policy is only $1.5 million. Term lengths are fairly standard and last between 10 and 30 years.

Bestow claims that customers can get quotes by answering only five questions. They also say that their policies start at just $11 per month.

While other insurance companies often require that you talk to an agent over the phone to finish the application, Bestow says their entire application process is 100% online.

If you do pass away while your policy is active, your beneficiaries can receive free access to a grief support group.

Bestow offers a 30-day period during which time you can cancel the policy and get your money back.

FAQs

Yes, Everyday Life is an insurance broker rather than a direct provider. This means that it doesn’t underwrite its own policies, but instead recommends policies from a mix of providers that may be suitable to your needs and application.

Everyday Life doesn’t charge a fee for you to be matched with potential providers. However, since it’s not a direct provider and because life insurance is so personalized, policy amounts may vary depending on which provider you choose and your personal health and circumstances.

Summary

Applying for life insurance with multiple companies can help you find the lowest rate for the right amount of coverage. And unlike applying for a loan or credit card with multiple companies, getting several different life insurance rates will not affect you negatively in any way.

Also, Everyday Life’s Predictive Protection model can help you buy just the right amount of insurance so you don’t overpay or don’t have enough coverage.

The post Everyday Life Insurance Review 2024 appeared first on Best Wallet Hacks.

]]>The post How to Start a Business appeared first on Best Wallet Hacks.

]]>When it comes to building wealth, you can go the traditional route: Get a job, invest 10% of your earnings, and retire at 65 with a decent nest egg.

Some people, however, want to be more creative in the hopes of generating more wealth. Maybe they decide to buy a rental property and become landlords or run an Airbnb.

One of the most common ways to build lasting wealth? Start a business.

But starting a business is not for the faint of heart – despite what social media might say, it is harder than it looks. Research from the Bureau of Labor Statistics found that almost 20% of small businesses fail in their first year. About half will fail after five years, and a staggering 65% will fail within 10 years.

So if you’re still interested in starting your own business, read below to see what steps to take to ensure your business is set up for success.

Table of Contents

- Define Your Idea

- Research Competitors

- Create a Business Plan

- Find a Community

- Choose Your Business Structure

- Get Legal

- Open a Business Bank Account

- Fund Your Business

- Using Your Own Money

- Taking Out a Business Loan

- Relying on Invoice Financing or Factoring

- Open a Business Credit Card

- Equipment Financing

- Start a Crowdfunding Campaign

- Manage Business Finances

- Apply for Business Insurance

- Come Up with a Name

- Find Your Customers

- Final Thoughts

Define Your Idea

Your idea is the foundation for your business. Without a solid idea in place, the rest of your business will crumble. Coming up with your idea can be the longest part of the process, especially if you don’t already have something in mind. Here are some ways to come up with a strong idea that can stand the test of time:

Determine What Your Idea Is

Before you can start filing your business registration or getting the necessary licenses and permits, you need to figure out what your business idea is. You should try to be as concrete as possible. This will also help you determine who you’re targeting, how you’ll market it and how to price your products or services.

Your business does not necessarily have to be groundbreaking to be successful. There are plenty of businesses that are very similar. However, you do have to offer a service or product that people are willing to pay for. You may need to conduct market research to figure out what product or service to offer and who the ideal client is.

If you don’t already have an idea, take some time to brainstorm. You don’t have to settle on just one idea. If you have a few, you can test them out before determining which one is the most likely to work in the real world.

Once you have an idea, consider talking it over with other people and getting their feedback. If their response isn’t as positive as you would have hoped, don’t despair. Use their comments to help you refine and shape your idea.

Sometimes though you have to ignore other people, especially if they’re not offering constructive criticism and are simply being negative.

Here are 11 side hustles you can start for less than $100 if you need some inspiration.

Fill a Need

Many people launch successful businesses by recognizing a need in the market and then working to fill it. For example, the creator of Spanx, Sara Blakely, used to cut her pantyhose to create custom shapewear that gave her body a perfectly smooth look. After some time cutting pantyhose, she realized that she could create her own product to solve her shapewear needs. Thus, Spanx was born.

If you’re trying to start a business, try to fill in the blanks in the sentence: “I help ___ with ___.” For example, if you want to start a mobile dog grooming business, you could say, “I help busy dog owners with grooming services like washing, nail trimming, and grooming.”

Buy a Franchise

If you want to be a business owner but don’t have a specific idea of your own, you could buy a franchise location.

A franchise requires you to put down a chunk of money to own a location of a well-known and established brand. Having a franchise means you do not need to have a business idea because you already know what the business is. If you’re dead set on becoming a business owner but can’t come up with an original idea, then owning a franchise might be a good alternative.

Buying a franchise though isn’t cheap. Want to own your own McDonald’s location? You’ll need about $750,000 in liquid assets. Data from the International Franchise Association says that the typical franchise down payment is $250,000.

If you don’t have that kind of money, there are plenty of less expensive franchises. For example, 360 Clean is a commercial cleaning franchise you can buy for only $15,000. You can also take out a loan for the franchise fee.

A benefit of a franchise is that it comes with operations already figured out. All you have to do is work the already established system.

Become a Freelancer

If you have a specific skill, perhaps from your day job, you can start doing that on your own.

For example, you can become a freelance marketer or advertising copywriter. Doing this yourself can help you discover if you actually like being your own boss or if you want to go back to being a regular employee.

As you get more and more business, you can start hiring someone else on an hourly or part-time basis. Starting off as a freelancer instead of immediately diving in with a full-service agency and several employees can minimize risks.

Here’s our ultimate guide to freelancing to help you get started.

Research Competitors

Once you decide on your business idea, you need to determine your competition. This depends on your business. For example, if you are trying to start a craft brewery, your competitors are other craft breweries in the area, not major beer companies like Miller.

But if you’re trying to start a jewelry business, then your competitors may be national and global brands, as well as local businesses.

One of the best ways to research the competition is to conduct a SWOT analysis. A SWOT analysis stands for:

- Strengths

- Weaknesses

- Opportunities

- Threats

By doing a SWOT analysis, you can find potential problems that could derail your business before it even begins. You may be able to hire an outside party to do the SWOT analysis for you. When you’re a business owner, it can be tough to distance yourself enough to be objective about your business.

Create a Business Plan

When you’re starting a business, it’s important to know how much it will truly cost to run a successful business. A business plan can outline your projected expenses and income so you can determine future cash flow projections.

A business plan may look different depending on the business and how detailed you want to be. In general, you should include how you plan to earn money and how much you will have to spend to keep the business running. If you need to take out a loan, then your plan should also factor in how long it will take to pay off your loan.

It can take a while to come up with a solid business plan and you may need to revise the plan if the industry changes.

It should also have goals for certain intervals, like a one-year and five-year goal, etc. Remember, these should be educated guesses rooted in reality.

Find a Community

Starting a business can be a lonely endeavor. One of the best ways to increase your odds of success is to find a community of like-minded people. You can do this on social media or even in person.

Joining your local Chamber of Commerce can be an easy way to find other business owners that you can learn from or collaborate with. They often offer a free trial period where you can sit in on meetings without paying to become a full-fledged member. You may also receive discounts on other services if you’re a Chamber member.

Don’t shy away from business owners who happen to be your competition. For example, if you are a bookkeeper, feel free to make friends with other bookkeepers. No one can serve every customer, and your best referrals will likely come from those you consider the competition. They can also give you great tips for being more successful.

Get a Mentor

Having a mentor, especially one in a similar field, can help you get started if you’ve never had a business before or are delving into a new industry.

Finding a mentor can be challenging, especially depending on the type of business you’re in. You can start by reaching out to successful people you know, sharing what your business is, and asking them if they know anyone who can help.

If you go with this strategy, make sure that you start by contacting people who know you well. Remember, no one will refer you to someone unless they can vouch for you.

Take some time to think about who you can ask to be a mentor. You can also look through your high school or college alumni list and find people in a similar industry. If you do reach out to them, ask if you can buy them coffee or lunch in exchange for answering some of your questions.

Before showing up, make sure to have a specific list of questions prepared. Don’t bring questions that you can answer via a Google search. If you don’t come off as polished and professional, you’ll kill your chances of finding a mentor.

LinkedIn can also be a powerful way to find a mentor. If you find someone that you have a mutual connection with, you can ask that person to refer you.

Choose Your Business Structure

The best legal structure depends on what kind of business you have. For example, if you want to start a personal training business, then you may want to operate as an LLC to ensure that a client who gets injured during a workout can’t come after you personally.

You are not bound to the specific type of business structure you selected when you first opened. However, changing structures can cost money, as you may have to pay an extra filing fee. Many business owners start out as a Sole Proprietors and eventually move to an LLC or S-corp.

If you’re having trouble deciding what kind of structure fits you best, you can speak to a CPA who can help you run the numbers. You can also speak to a business attorney who can suggest which structure will offer you the most protection.

Sole Proprietorship

A sole proprietorship is the easiest way to start a business. It means that you’re essentially working by yourself.

Working as a sole proprietor is simple because you don’t need to file paperwork with the state or federal government. However, the downside is that you don’t have the same legal protections as an LLC. As a sole proprietor, your personal assets are on the line if someone decides to sue your business — even if you’re not working out of your home.

Being a sole proprietor also provides the least amount of tax savings as a business owner.

Partnership

If you’re starting a business with someone else, you could set up a partnership. A partnership is basically a sole proprietorship, but with more than one person.

It is similar to a sole proprietorship in terms of how it reports income on your taxes.

LLC

A Limited Liability Corporation (LLC) is a business structure that protects business owners from having their personal assets touched if they’re involved in a lawsuit. If you own an LLC, the profits can be passed onto your personal income.

Filing as an LLC involves an extra fee. Also, as of 2025, LLC businesses must file a Beneficial Ownership Information (BOI) form. This form is fairly straightforward and only takes a few minutes to complete. However, if you don’t complete it, you could wind up paying a hefty fine.

S-Corp

An S-corp is a business structure that passes through its profits to shareholders. If you have an S-corp, you may be able to take advantage of some tax savings.

An S-corp can still have an LLC structure so the owner isn’t liable for the business in case of a lawsuit.

✨ Related: How to Pay Yourself as a Business Owner

Corporation

A corporation is one of the more complex types of businesses you can open. There are separate corporation filing fees.

Corporations can have shareholders who each own a different percentage of the business. This structure is for very large companies that will be selling shares.

Get Legal

One of the first things you’ll have to do when starting a business is ensure that you’re following all applicable laws. If you’re not legally registered, then you will almost certainly have trouble getting funding, because lenders don’t want to give money to an unauthorized operation.

Get a License

When you start a business, you often need to get an official license that lets you do business in your state. The type of license will vary depending on the type of business you have. For example, if you want to start a bar, you’ll need a liquor license. If you want to turn your basement into a private pilates studio, you may need a specific business license.

If you’re not sure what kind of business license you need, you should contact your state government or local Small Business Administration. They can help you figure out what you need to be legal.

In some cases, you may also need to register your business federally. This comes with its own set of paperwork that can take time to complete correctly. Alternatively, you can also pay a service to do the work for you.

EIN

No matter what kind of business structure you have, you should get an Employer Identification Number (EIN). Think of this as a Social Security Number for your business. This unique number can be used when filing your taxes, applying for funding, and more.

You can get an EIN for free from the IRS. Make sure to use it on your official business documents. It only takes a few minutes to complete the form and get your EIN.

Using an EIN can also protect you from identity theft. If you use your SSN on business documents and this paperwork is stolen, then you will have to monitor your credit and ensure that hackers don’t use your SSN to engage in fraud.

Open a Business Bank Account

As a small business owner, it’s important to keep your business finances separate from your personal finances. Therefore, you will need to open a separate business bank account. This will make it so much easier when you start looking for business funding because you’ll be able to provide business bank statements that show how much money is coming in – and how much is going out.

This will also simplify your tax filing process because you’ll know what your business expenses are and what expenses are personal.

Many banks and credit unions offer business bank accounts, including both checking and savings accounts. You can choose from a national bank, a smaller regional bank, or a credit union.

When comparing banks, try to pick one with the fewest fees possible. If you’re tech-savvy, you should also try to find a bank that offers a mobile app with decent reviews. This can ensure that you’ll be able to deposit checks via the mobile app, check your balance on the go and more.

Sometimes regional and local banks and credit unions may offer good interest rates and low or no fees for business accounts. These smaller banks may also be more likely to lend money to new businesses.

You can use a business savings account to save money for a rainy day, buy new equipment, and more. Look for a business savings account boasting a decent interest rate.

Here’s our list of the top business bank accounts.

Fund Your Business

Every business — no matter the idea — needs money. And funding a business is one of the most common roadblocks.

There are two basic ways to fund your startup costs: get it from someone else or use your own money.

If you go with the latter option, that might include:

- Withdrawing money from your 401(k), IRA or other investment account

- Withdrawing money from your checking or savings account

- Taking out a home equity loan or line of credit

Depending on the business, you may also be able to bootstrap it. This means starting small and investing the profits back into the business until it grows enough to start taking an income.

Using Your Own Money

There are obvious downsides to using your own money. If your business goes under, you’ll have nothing left to recoup.

Also, there may be fees and fines associated with using your own money. For example, if you withdraw money from a tax-advantaged retirement account, then you may have to pay an extra fee. Withdrawing money from your traditional IRA or 401(k) will result in a 10% early withdrawal fee. You’ll also have to pay income tax on the amount.

A home equity loan can be easier to get because it uses your home’s existing equity as collateral. Here’s how that works. Let’s say you have a $100,000 mortgage balance on a home worth $500,000. In this case, you have $400,000 in equity. You can usually take out around 80% of a home’s equity, either as a loan or a line of credit. This would equal $320,000.

This amount could be significantly higher than what you could receive with a traditional business loan, especially as a brand-new business.

The downside of a home equity loan is that your home is then collateral for the loan. If your business tanks and you can’t afford to make the new payments, your home could be foreclosed upon. This would also ruin your credit and cost you thousands in extra fees and penalties.

Taking Out a Business Loan

Lending options for businesses are generally more limited than they are for personal expenses. For example, you can’t take out a personal loan for business expenses.

If you qualify for a business loan, you will still need to guarantee the loan personally. That means that if the business defaults on the loan, the lender will come after your personal assets. It can take years or even decades before a lender won’t require a personal guarantee.

Business loans can be obtained directly from banks, credit unions, or online lenders. Rates vary depending on the loan amount, type of business loan, and whether it is a fixed or variable interest rate.

A business loan can have a term ranging from one year to 20 years, with longer terms often having higher interest rates. You can also apply for a business line of credit, which lets you draw upon a line of credit over a specific period of time. Once the draw period ends, you will have to pay back any outstanding balance.

Loan amounts can start as low as $1,000 and end at $1 million. The amount you qualify for depends on your credit score, time in business, number of employees and more.

Relying on Invoice Financing or Factoring

If you send invoices to customers and they take too long to pay, you could wind up making late payments to your own vendors. That’s where invoice financing or factoring comes in.

This funding strategy involves essentially selling an invoice to a third-party company, who will give you around 80% of its total value. When the client finally pays the invoice, the third-party company will receive the funds.

While this method means you’ll earn less money than you would if you waited for payment, it also ensures that you can still pay your own bills.

Open a Business Credit Card

Like regular consumer credit cards, business credit cards are fairly easy to open, even if your business is barely operational. Business credit cards typically come with a high credit limit, the average is around $50,000.

When you have a business card, you can pay your vendors, buy equipment and purchase supplies. I like the Chase Ink Business Cash® Credit Card.

Business cards are often personally guaranteed, so your credit will be impacted if you don’t make the payments.

Equipment Financing

The toughest part of business financing is when your business doesn’t have physical items to use as collateral. But if you have equipment, you may be able to qualify for equipment financing in lieu of a traditional business loan.

Interest rates for equipment financing are usually less than they would be for a regular business loan. The repayment term is usually between three and 10 years, and rates are often fixed for the duration. You may be able to get equipment financing through the dealer where you bought the equipment.

Start a Crowdfunding Campaign

In the last few years, starting a business with a crowdfunding campaign has become a viable option. Here’s how it works: You decide how much you want to raise, write why you need the funds, and launch the campaign. If you reach your goal, you keep the funds without having to pay them back. Sounds easy, right?

Unfortunately, crowdfunding campaigns aren’t a given. The success rate for a crowdfunding campaign – business or personal – is around 20%. And if you don’t raise 100% of the stated goal, then you will have to return all the money raised.

Relying on a crowdfunding campaign can use up lots of your social capital. If people try to raise money for you and the campaign fails, they may be hesitant to financially support you in the future.

Manage Business Finances

Being a small business owner comes with a whole new challenge: taking care of your business finances. Here’s what to know about taking care of the financial side of owning a business:

Track Income and Expenses

When starting a business, it can be easy to lose track of your spending. But not knowing how much money is coming in or going out can make it harder to determine whether you’re actually making a profit.

That’s why it’s imperative to use accounting software, like Quickbooks, to manage your business finances. Again, business taxes are also more complicated than personal taxes so it’s wise to set things up correctly from the beginning.

At some point, you may need to hire an outside party to handle your bookkeeping and/or taxes. If you already have a system in place, it will be much easier — and less expensive — for them to sort through your finances.

If you have a business that charges state taxes, you will have to set aside those funds until it’s time to pay the state. Make sure to keep this in a separate account so you don’t accidentally spend the money.

Apply for Business Insurance

When you are a business, you are often exposed to legal risks, such as being sued. Even if you think that your business is safe from legal issues, you may need to buy business insurance to protect you.

For example, if you’re trying to start a private practice as a physical therapist, then you will likely need malpractice insurance to cover you in case someone is injured under your care. Even just renting an office could mean you need liability insurance. You may also want to consider a bond to protect you against claims of theft or fraud.

When choosing a business insurance policy, make sure to compare different providers. Different companies may have different pricing methods that can vary significantly.

You should also be completely honest and describe how your business operates so the insurance company knows how to quantify your potential risk factors. You can also keep shopping around even if there is an existing policy in place.

If you have employees who work for you, you may need to verify that you have the right type of insurance to protect them in case something happens. For example, you’ll need a workers’ compensation policy if you have employees.

Property Insurance

If you buy a building or land for your business, you should insure that property. Just like a homeowner’s insurance policy, this type of insurance will help you recoup your losses in case of damage like fire, storms and more.

When buying a policy, your property will need to be appraised. If you do any property improvements, you will have to upgrade your policy.

Product Liability Insurance

If you are building a product to sell, you may want to purchase product liability insurance. This can protect you in case your product is defective and accidentally hurts someone.

For example, let’s say you manufacture children’s toys. If one of your toys breaks and hits the child in the face, the parents could come after you if there are any injuries. While this may sound like a ludicrous hypothetical, it’s always better to be overprepared.

Vehicle Insurance

Whether you use a specific company vehicle or your own personal vehicle for business purposes, you will likely need to buy a vehicle insurance policy for your business. This policy is separate from your personal car insurance, which only covers you if you use the car for business purposes.

If you don’t have business insurance and get into an accident, you could end up having to cover all those costs yourself—even if the accident isn’t your fault. It’s similar to driving around without car insurance.

Come Up with a Name

One of the most important factors to consider when choosing a business name is its SEO potential. You need to choose something that is unique and not too similar to your competitors.

For example, if you wanted to start a diner, you wouldn’t want to use the word “waffle” in your name, because it might be compared to “Waffle House.”

Once you have a name in mind, type it into Google and see what comes up. It’s almost impossible to find a unique business name, but you should try to find a name that can stand out on Google. If your business is locally-minded, then double-check that there isn’t a similar business with the same name in your area. That would make it harder for people to find you online.

You also want a business name that is easy to remember and has some kind of connection with your service or product. For example, if you want to start a landscaping business, a name like “Marcy’s Landscaping” is more direct and helpful than just “Marcy’s.”

You should also check to see if you can buy the domain for your business name and claim the social media accounts.

Find Your Customers

Once your business is set up and running, you can start finding your potential customers.

Create a Website

Nowadays, having a web presence is essential for business success. Without a website, you may struggle to build a clientele or find funding.

For many types of businesses, you don’t need a web developer to build a website. You can use a service like Squarespace or Wix to build a professional-looking website that will attract customers.

If you plan on selling items directly through your website, you can connect with third-party services like Shopify that will take care of some of the back-end for you. Some businesses can also use third-party sites, like Etsy or Amazon, to sell their wares.

If you’re not sure what kind of website setup you need, look at your competitors and see what they’re doing. If you have mentors in the space, you can also ask them how they operate and what they would recommend if you’re just starting out.

Some types of websites are better for fully established businesses, while others are more appropriate for newly launched businesses.

Utilize Social Media

One of the best ways to find customers is to utilize social media. Having a strong social media presence can give your business more legitimacy, especially in the beginning before you have any word of mouth. If people see that your business has a consistent social media posting schedule, they may treat you more like a legitimate enterprise instead of a scam.

Try to post to social media platforms that your customers use regularly and don’t spread yourself too thin. For example, if you’re targeting those in their 50s, you don’t need to start a TikTok account. That would be a better fit for those trying to appeal to teens and young adults.

Start by choosing one or two platforms that you know how to use and post on them regularly. The algorithm promotes accounts that are more consistent. Once you master those networks, you can decide to add more accounts if you’re comfortable. You can also hire someone to manage your social media for you.

Don’t forget that you can also rely on your personal social media and web presence to sell your business. If you have a strong presence already, then those people may be willing to support your business.

Network in Person

Meeting potential customers in person is a great way to test your business idea. For example, if you’re creating a product, you can go to local fairs and set up a booth. This can be an easy way to see how people respond in real life. You might even get inspiration for other ideas just by being out in the real world.

You can find local business-minded meetups or attend local conferences and other events where you can meet potential investors, shareholders, and customers.

Final Thoughts

You should also realize that starting a business will require more time, emotional energy, and dedication than working a 9-to-5. Most new business owners don’t realize that starting a new business is like having a baby. It takes a lot of time for the business to become self-sufficient, and there may be steep learning curves. And just like it helps to have a babysitter or a helpful mother-in-law on call, your business will almost certainly need help from other people.

Some people think that having their own business is easier than working for someone else because they don’t have to report to anyone else. But even when you’re a business owner, you still have to answer to customers, employees and, if you’re lucky enough, investors. You’ll be pulled in a million different directions.

A survey found that 56% of business owners have anxiety, depression, or another stress-induced illness, while 75% of small business owners are worried about their mental health. If you don’t have the bandwidth to take that on, then starting a business may not be for you.

Also, if you have a family, you need to consider how starting a business will affect them. Will your spouse have to become the sole provider for awhile? Will you have to cut back on retirement savings or contributions to your child’s college fund?

Answering these questions first can help you decide not only if you’re up to having a business but also what kind of business you want to start.

The post How to Start a Business appeared first on Best Wallet Hacks.

]]>The post How to Lower Your Cell Phone Bill: 10 Ways to Save appeared first on Best Wallet Hacks.

]]>My cell phone bill is one of the larger utility bills I pay. I use cheaper cable TV alternatives and now pay just $12 monthly to watch TV.

With four teenagers in the house, I assumed I was stuck paying a giant cell phone bill. However, I found a way to cut costs. I’ve compiled the following list of 10 ways to lower your cell phone bill. You can try one, two, or more of these money-saving ideas. The best part is that most options won’t affect your cell phone services.

Table of Contents

1. Switch Carriers

Switching mobile carriers doesn’t always mean lower-quality cell service. In fact, some discount mobile carriers are owned by the largest carriers: T-Mobile and Verizon.

In addition, most discount mobile carriers use big-name networks to connect anyway. Here are three discount mobile carriers that may be able to save you money.

Mint Mobile

Mint Mobile has been offering discount cell phone plans since 2015 and was acquired by T-Mobile in 2023.

The carrier offers four different plans:

- 5GB of data for $15 per month

- 15GB of data for $20 per month

- 20GB of data for $25 per month

- Unlimited data for $30 per month

Mint Mobile also offers family plans for even deeper discounts. For more information, check out our Mint Mobile review.

Visible

Visible is a discount cell phone carrier that is owned by Verizon. This carrier has just two affordable plans:

- Unlimited talk, text, 5G/4G LTE, and hotspot for $25 per month

- Unlimited talk, text, 5G Ultra, and hotspot for $45 per month

Learn more in our full Visible review.

Tello Mobile

Tello Mobile is an independent discount carrier operating on the T-Mobile network. The carrier offers a “build your own” phone plan system with as little as 0 GB of monthly data.

For instance, you can get a talk-only plan with no data and no text minutes for just $5 per month. Or you can get unlimited data and unlimited talk and text for just $25 per month.

2. Get on the Right Plan

If you’re not interested in switching to a different service provider, you may be able to save money on your phone bill by ensuring you have the right plan for your usage.

Start by reviewing your monthly phone bill. How much data are you using? Do you regularly exceed your data limits? Or is your data usage significantly less than what your plan allows for?

Check to see if your carrier offers a more suitable plan for your usage. If so, contact them and make the switch.

✨ Related: How to Lower Your AT&T Cellphone Bill

3. Skip the Phone Upgrade

Most wireless carriers make a habit of offering phone upgrades every few months. They’ll send you an ad with a shiny new phone and offer you a discounted “sale” price.

Your carrier may even offer “affordable” monthly payments on the upgraded phone. Don’t fall for the temptation of new and shiny, especially if your current phone is working just fine.

Instead, use your current phone as long as you can. Don’t feel like you’re missing out on bells and whistles; the novelty wears off very quickly.

Keep your financial goals in mind and remind yourself how much faster you’ll reach them if you don’t upgrade to a new phone.

4. Sign up For Autopay

Almost all cell phone carriers offer a discount if you sign up to have your bill paid via autopay. In fact, you may be able to save 5%, 10% or more. Using autopay can also make budgeting easier by ensuring you’re not late with your bills.

5. Reassess Your Cell Phone Insurance Plan

Does your phone plan include an optional insurance policy? If so, consider canceling the insurance.

If you’re worried about losing or damaging your phone, start setting a few dollars aside each month for a replacement. That way, you’ll have the cash to buy another phone when needed.

Also, check your credit card. Many cards include cell phone insurance if you use it to pay your bill.

Mastercard World Elite products are the most likely to offer free cell phone protection of up to $800 per claim (a $50 deductible applies) against theft or damage when charging your monthly phone bill to your credit card.

Another option is the Chase Freedom Flex. It offers $800 in coverage per claim, a $50 deductible. It has a $1,000 per year limit.

Finally, your homeowner’s insurance or renters insurance policy may cover some claims too.

Know, too, that most phone accidents are avoidable. Purchase a durable case and screen protector, and take special care not to damage or lose your phone so it has a better chance of lasting longer.

6. Join a Family Plan

Having more than one person on your phone plan is another way to lower your cell phone bill. For this reason, check into family plans if you live in a multi-family member household.

If you don’t, discuss joining a family plan with trusted family members or friends. You can often sign up for a carrier’s family plan even if you and the others on your plan don’t live in the same house.

Be sure to set clear guidelines about how a family plan will be paid for, especially if you’re joining with friends, adult family members, or those who don’t live in the same household.

✨ Related: 8 Cheapest Family Cell Phone Plans

7. Use Wifi When Available

Nowadays, most employers and retailers offer free Wi-Fi services, which means you can use wifi almost everywhere you go.

Use it when available, and save your data for when you have no other options. Or, decide not to use your phone where Wi-Fi isn’t available unless it’s an urgent matter.

See if your efforts help you reduce your data usage. Then, consider switching to a cheaper plan with less available data.

8. Ask for a Better Deal

It never hurts to call your cell phone carrier and ask for a better deal. Before you call, check online to find out what competitors are offering if you switch.

Once you’ve found a great deal, call your carrier and politely explain that you’re seeing a better deal and would like information about canceling your service.

Since customer service reps are often trained to give discounts to customers who want to cancel, you might automatically be offered a better deal. If not, tell them you’d like to stay with their company and ask for a better deal.

9. Join a Bill Trimming Service

Have you ever used a bill negotiation service like OneMain Trim? It’s one of several AI apps that can save you money with little to no effort.

When you link cards and accounts to the app, OneMain Trim quietly works in the background, searching for monthly, annual, or other subscriptions. The app then asks you to keep the subscription.

If you don’t, OneMain Trim will cancel the subscription on your behalf. And if you want to keep the subscription, OneMain Trim will work to negotiate a better price.

OneMain Trim doesn’t charge any monthly or annual fees. However, it charges a yearly fee of 15% of any money it saves you. If there are no savings, there is no cost to you.

10. Go Minimalist

Finally, you can save big by taking a minimalist approach to your phone. Instead of paying to access every possible feature, consider what is absolutely essential and what you could do without.

For instance, do you need the nicest cameras or the most memory? Can you live with a slightly smaller screen? The fewer bells and whistles your phone has, the less you’ll spend on it. Once you’ve settled on a phone, choose the cheapest plan that suits your needs.

FAQs

Discount carriers often offer service equal to the full-price carriers. Your best bet is to read online reviews and see what quality of service others are experiencing with discount carriers. Also, make sure the discount carrier offers solid coverage in your area.

Most services allow you to keep your current phone number when you switch cell phone service carriers. However, if you want to keep your number, always ask before you sign up with a new carrier.

Before you purchase a used cell phone, ensure that it’s unlocked. Locked phones are tied to a single carrier, while unlocked cell phones can be used at multiple carriers. Keep in mind that carriers usually only work with select types of phones, too.

No, your phone doesn’t have to be paid off before you switch carriers. That said, know how much you’ll pay in fees and interest if you leave your carrier before your phone is fully paid. Your carrier will likely penalize you financially if you leave before paying for your phone.

Final Thoughts

For many, knowing how to lower a cell phone bill is a big step toward staying on budget and progressing with your financial goals. And, as you can see, there are plenty of ways to do it. Choose the phone and the phone plan that best fits your needs, and watch your bank account grow.

The post How to Lower Your Cell Phone Bill: 10 Ways to Save appeared first on Best Wallet Hacks.

]]>The post Bilt Rent Day Promotion April 2024: Free Fitness Classes appeared first on Best Wallet Hacks.

]]>If you pay rent, you need to know about Bilt.

The Bilt Mastercard is a no annual fee credit card that lets you earn rewards (up to 100,000 points a year!) when you pay your rent by credit card.

In addition to earning rewards for paying rent, they offer plenty of other nice features and promotions. One of them is called Bilt Rent Day, which is a rotating promotion active on the first of every month.

We will update this post each month with the latest Rent Day promotions as we learn about them.

Table of Contents

What is Bilt Rent Day?

Bilt runs a different promotion on the first of each month, known as Bilt Rent Day. The promotion varies each month.

They are generally active from 12:00 AM Eastern time until 11:59 PM Pacific time to encompass the entire United States, so you technically have 27 hours to take advantage of the offer.

If you want to learn more about Bilt, our Bilt review digs deeper into all the program’s benefits (of which many extend beyond Bilt Rent Day).

For April 2024, they expanded their fitness partnerships:

April 2024: More Fitness Partners + Complimentary Classes

Bilt always had partnerships with SoulCycle and Y7, but they’ve now added AKT, BFT, CycleBar, Pure Barre, Row House, and Rumble Boxing.

As part of Bilt Day, when you book an upcoming fitness class, you will get a complimentary class credit when you are in the Blue or Silver tier. Gold and Platinum Status members will get 2 free class credits per booking. You can use the free credit within 90 days of April 1st.

You can also book free classes for Rent Day, limited availability so log into your Bilt account and see what is still available. (Update: these classes have all been booked up)

You can still play Rent Day – their monthly game where you can win points, free rent, etc:

April 2024: Earn bonus 2-6x Bilt Points

This offer is included each month (as far as I can remember).

Typically, you earn 1x on rent payments, 2x on travel, and 3x on dining when you use the card 5 times each statement period. On Rent Day purchases, you earn double the rewards on dining, travel, and all other points, excluding rent (on which you still earn 1x points).

That’s 6x on dining, 4x on travel, and 2x on everything except for rent.

They also limit you to 10,000 bonus points each month; you still need to use your card at least five times to earn these points.

Previous Bilt Rent Day Promotions

Are you curious about what they offered in previous months?

They typically offer double bonus points on dining, travel, and non-rent purchases each month.

This list shares the “other” bonus promotion:

March 2024: Earn 2,000 bonus points linking cards

(For March, they used a March Madness bracket and had everyone vote for which promotion would win out… and it was this one)

Unlike in other months, which featured point transfer bonuses, March 2024 features a bonus when you link another credit or debit card to your Bilt account. You get 1,000 points per card for up to two cards, which had to be previously not linked to your account.

If you were Gold or Platinum, you could also decide to take the runner-up reward, which was earning 5X at grocery stores.

February 2024: Transfer Points to Air Canada Aeroplan